Private Dental Insurance for Over 50s: Is It Worth the Cost?

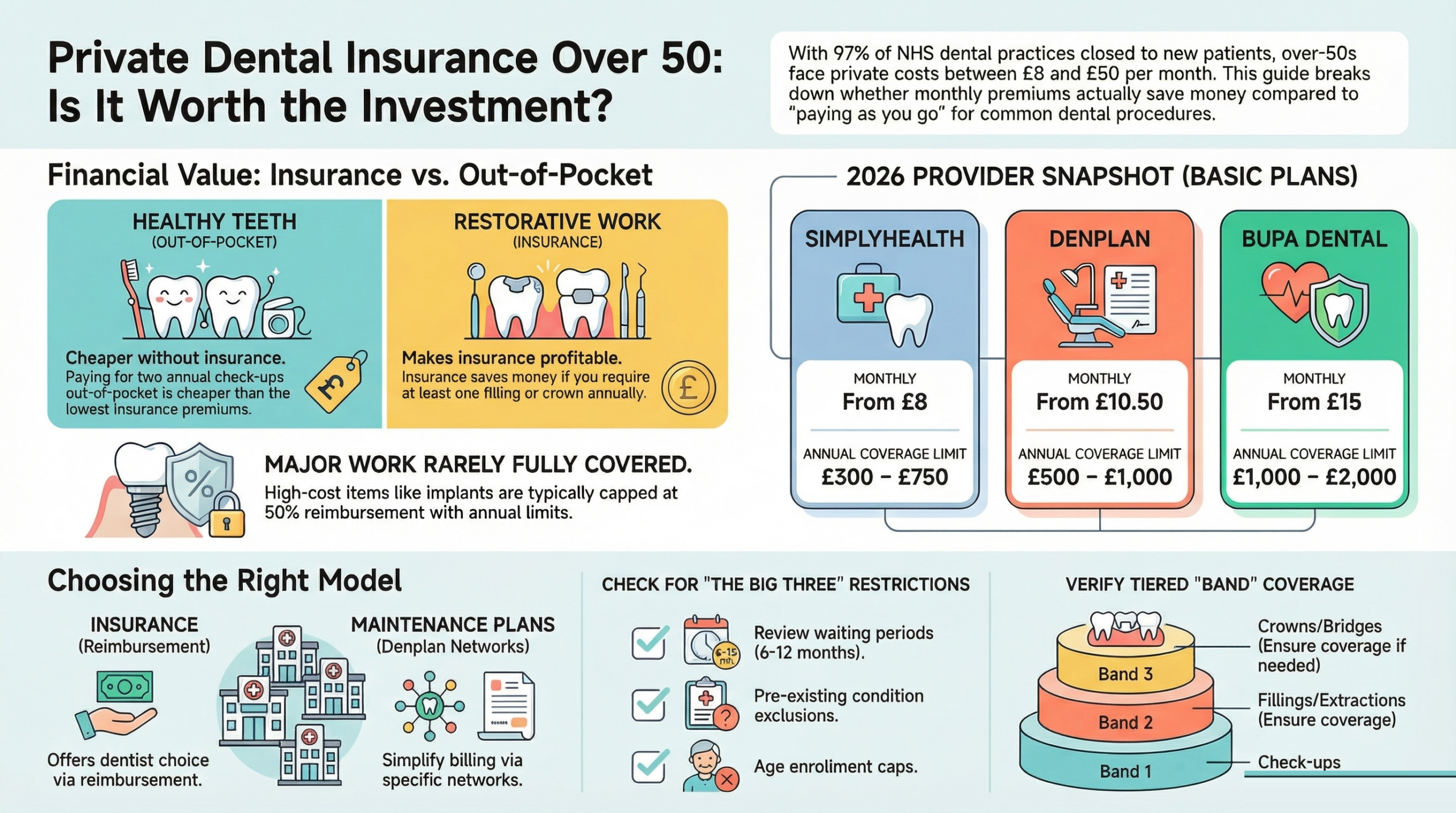

Getting dental care in the UK has become increasingly difficult. With 97% of NHS dental practices now closed to new patients, many adults over 50 are turning to private dentistry-and wondering how to afford it. Private dental insurance for over 50s can cost between £8 and £50 per month, depending on the provider and coverage level. But does it actually save you money compared to paying as you go? This guide compares the leading plans from Bupa, Denplan, Simplyhealth, and AXA, explains what you’re really getting, and shows you how to work out whether insurance makes sense for your dental needs.

How Much Does Private Dental Insurance Cost for Over 50s?

The cost of private dental insurance varies widely. Your age, existing dental health, and the level of coverage you choose all affect the premium. Here is a breakdown of the main providers available to over-50s in 2026:

| Provider | Basic Plan | Standard Plan | Premium Plan | Excess / Limits |

|---|---|---|---|---|

| Denplan | From £10.50/month (routine only) | From £17.50/month (includes Band 2) | From £30/month (includes Band 3) | No excess; annual limits £500-£1,000 |

| Bupa Dental | From £15/month (routine) | From £25/month (includes fillings) | From £50/month (major dental) | £100 excess; £1,000-£2,000 annual limits |

| Simplyhealth | From £8/month (preventative only) | From £13/month (includes restorative) | From £20/month (includes major) | No excess; £300-£750 annual limits |

| AXA Dental | From £12/month (routine) | From £22/month (includes fillings) | From £35/month (includes major) | £50 excess; £800-£1,500 annual limits |

Our guide to NHS vs private dentist costs compares NHS and private dentist costs side by side, with real UK prices for every common treatment.

All of these providers offer plans tailored to over-50s, though some have age limits (typically 60 or 65 for new customers). Denplan is technically a dental plan rather than insurance-you pay a monthly fee to a registered practice-while Bupa, Simplyhealth, and AXA are traditional insurance products that reimburse you for claims.

Watch: Private Dental Insurance for Over 50s – Is It Worth the Cost?

This cinematic overview walks you through the key decisions facing over-50s considering dental insurance, comparing monthly premiums from Bupa, Denplan, Simplyhealth, and AXA with real break-even scenarios to help you work out whether a plan makes financial sense.

What Does Dental Insurance Actually Cover?

Understanding what you are paying for is crucial. Dental insurance plans are typically tiered into three categories, mirroring the NHS Band system:

Preventative and Routine Care (Band 1)

This covers check-ups, cleaning, and scaling. All dental insurance plans cover Band 1 treatment, usually with 100% reimbursement. Most plans include up to two check-ups per year at no additional cost.

Fillings, Root Treatment, and Simple Extractions (Band 2)

Band 2 treatment covers restorative work like white fillings, root canal therapy, and tooth extraction. Most standard and premium plans reimburse 70-80% of Band 2 costs after your excess. A single filling might cost £75-£150 privately, depending on the tooth and material used.

Major Dental Work (Band 3)

This includes crowns, bridges, implants, orthodontics, and complex treatments. Only premium plans typically cover Band 3 work, and coverage is usually limited to 50% reimbursement with an annual cap. Dental implants, which cost £1,200-£2,500 per tooth privately, are often excluded or subject to waiting periods of 12-24 months.

Common Exclusions and Waiting Periods

Most plans exclude cosmetic dentistry (teeth whitening, veneers) and impose waiting periods before you can claim for major work. Pre-existing dental conditions diagnosed before you take out the policy are typically not covered, though some providers waive this for basic check-ups. Emergency cover abroad is rarely included in standard plans.

Key dental care facts at a glance – The Best of Health 2026

Find out more in our complete guide to NHS dental charges 2026, which explains exactly what NHS Band 1, 2 and 3 dental charges cover and who qualifies for free treatment.

Is Dental Insurance Worth It? A Break-Even Analysis

Whether dental insurance saves you money depends entirely on how often you need treatment. Let us work through two realistic scenarios for an over-50 adult:

Scenario 1: Good Oral Health

You visit your dentist twice per year for a check-up and clean, with no fillings or treatment needed.

- Private costs without insurance: 2 check-ups at £25 each = £50 per year

- Insurance cost: £10/month Simplyhealth plan = £120 per year

- Verdict: Insurance loses money. You would be better off paying as you go.

Scenario 2: Moderate Dental Work

You have two check-ups per year plus one filling and one crown every three years.

- Private costs without insurance: 2 check-ups (£50) + 1 filling every 3 years (£100) = £100 per year average

- Private costs in a year with a crown: Check-ups (£50) + filling (£100) + crown (£800) = £950

- Insurance cost: £22/month AXA standard plan = £264 per year (includes £50 excess on claims)

- Insurance reimbursement for crown: 50% of £800 = £400 (capped by annual limit)

- Verdict: Over time, insurance saves money, especially in years with major treatment. After 3 years: costs without insurance = £1,150; with insurance = £792 + £50 excess + claim processing = roughly £850-£900.

Scenario 3: Heavy Dental Needs

You require multiple fillings, root treatment, and possibly implant work.

- Single implant cost: £1,500-£2,500

- Insurance cover for implants: Rarely covered in full; typically 50% of Band 3 work with a £1,000-£1,500 annual cap

- Verdict: Insurance helps with routine and moderate treatment but does not fully cover expensive major work. A premium plan at £50/month (£600 per year) might cover half the cost of preventative care and fillings, but not large-scale implant work.

The key finding: dental insurance makes financial sense if you are likely to need at least one or two restorative treatments (Band 2 or above) per year. If your teeth are naturally strong and you have excellent oral hygiene, paying as you go will be cheaper.

Our guide to dental implants cost UK covers the full cost of dental implants in the UK, NHS eligibility criteria, and private pricing by region.

Dental Insurance vs Dental Plans-What Is the Difference?

It is important to understand the distinction between dental insurance and dental plans, because they work very differently:

Dental Insurance (Bupa, Simplyhealth, AXA)

You pay a monthly premium. When you have treatment at a private dentist, you pay the dentist upfront, then submit a claim to your insurer. The insurer reimburses you a percentage of the cost (typically 70-100% for routine, 50-70% for major work) up to your annual limit. This gives you flexibility to choose any private dentist, but you must wait for reimbursement and manage claims yourself.

Dental Plans (Denplan, Care Dental Plans)

You pay a monthly fee directly to the plan, which includes a network of dentists. There is no claim form or excess-you simply attend your registered practice and the plan covers the agreed treatment. Plans are simpler to manage but lock you into using dentists within the plan network.

For over-50s, dental plans like Denplan are often more attractive because they simplify billing and remove the worry of exceeding annual limits. However, if you have a strong relationship with a private dentist outside the network, insurance offers more choice.

What Should You Look for When Choosing Dental Insurance After 50?

Not all dental insurance is created equal. Use this checklist to find the best plan for your needs:

1. Annual Limits

Check the maximum amount the plan will pay per year. Plans with £1,000-£1,500 annual limits are standard; premium plans may go up to £2,000. If you need significant dental work, you could exceed this limit and pay the rest out of pocket.

2. Waiting Periods

Most plans impose a waiting period-typically 6-12 months-before you can claim for major work (Band 3). Some plans waive waiting periods for check-ups and fillings. Confirm this with your insurer before signing up.

3. Pre-Existing Conditions

If you have a tooth that needs treatment, check whether it is classified as pre-existing and excluded from cover. Some plans will exclude teeth with existing decay; others only exclude teeth that were treated before the policy started.

4. Age Limits

Most providers accept new customers up to age 60, with a few accepting up to 65. Once you are in the plan, you can usually continue until age 75 or beyond. Check whether there are age-related premiums-some insurers increase your premium as you get older.

5. Excess

An excess (or co-payment) is the amount you pay towards each claim. Plans with no excess (like Denplan) are simpler, but some traditional insurers charge £50-£100 per claim. This reduces the value if you have multiple treatments.

6. Emergency and Holiday Cover

If you travel or live abroad part of the year, check whether your plan covers emergency dental treatment abroad. Most basic plans do not; you may need to upgrade.

7. Cancellation Policy

Plans vary in how much notice you must give to cancel. Some require 30 days’ notice; others require up to 90 days. Read the small print if you think you may want to quit later.

Our guide to dentures cost UK compares NHS Band 3 and private denture prices, the different types available, and what affects the cost.

Frequently Asked Questions

Does private dental insurance cover treatment that I already need before I take out a policy?

No – most dental insurance policies exclude pre-existing conditions for the first 6-12 months, meaning any dental work you have been putting off will not be covered immediately. Always declare any existing dental issues when applying.

Are cosmetic dental treatments like teeth whitening covered by dental insurance in the UK?

Rarely – most dental insurance policies only cover routine check-ups, cleaning, emergency treatment, and restorative work like fillings and crowns. Cosmetic treatments such as whitening, veneers, and braces are usually excluded.

If I use my dental insurance to claim for a filling, will my premiums go up the following year?

Unlike some health insurance policies, dental insurance premiums typically do not increase just because you have made a claim. However, check your specific policy, as some providers may adjust premiums based on claim history.

If I have a dental cash plan instead of insurance, can I claim back all my private dental costs?

No – dental cash plans reimburse you up to a set annual limit (typically £200-£500 per year) for specific treatments like check-ups, hygiene appointments, and emergency care. They do not cover the full cost of major treatments like implants or complex restorations.

Key Takeaways

- Private dental insurance for over-50s costs between £8 and £50 per month depending on provider and coverage level.

- With 97% of NHS practices closed to new patients, private insurance is increasingly necessary for continuity of dental care.

- Insurance saves money only if you need at least one or two restorative treatments per year; good oral health means paying as you go is cheaper.

- Denplan (a monthly plan) and traditional insurance (Bupa, Simplyhealth, AXA) offer different benefits: plans are simpler but limit your choice of dentist; insurance is more flexible but requires claims management.

- Always check annual limits, waiting periods, excess, and age limits before committing to a plan.

- Major work like implants is rarely fully covered; you may pay 40-50% out of pocket even with insurance.

If you are considering private dental insurance, start by listing your realistic dental needs over the next three years. Will you need fillings, extractions, or major work? Once you have an idea of costs, compare the reimbursement rates and annual limits of at least three providers. The cheapest plan is not always the best value if it has low annual limits or long waiting periods. if you have not yet exhausted NHS options, but if you cannot access NHS care, a well-chosen insurance plan or dental plan can provide peace of mind and predictable costs.

Next Steps: Request quotes from at least three providers using your age and current dental health. Compare the annual limit, excess, and waiting periods-not just the monthly premium. Consider switching to a dental plan like Denplan if you want zero excess and simpler management. if you think you may need major work in the future.

Disclaimer: This article is for information only. Always consult your GP or a qualified dental professional before making health decisions. Costs and policy details are correct as of March 2026 but may change. Always confirm current premiums, limits, and waiting periods directly with the provider before applying.