A Guide to What Steps to Take if You Are Injured on Holiday

Holidays are a wonderful time of year, but things can swiftly turn sour if you suffer an injury. For over-50s, the risks are higher-falls, fractures, and medical complications can escalate quickly abroad. Minor problems tend to be easily remedied, but serious injuries can ruin your getaway and cause long-term health issues. If the worst happens when you’re away, it’s crucial to know exactly what steps to take. This guide covers your immediate actions after a holiday injury, how to use GHIC and travel insurance, the real costs you might face, and how to claim when you return home.

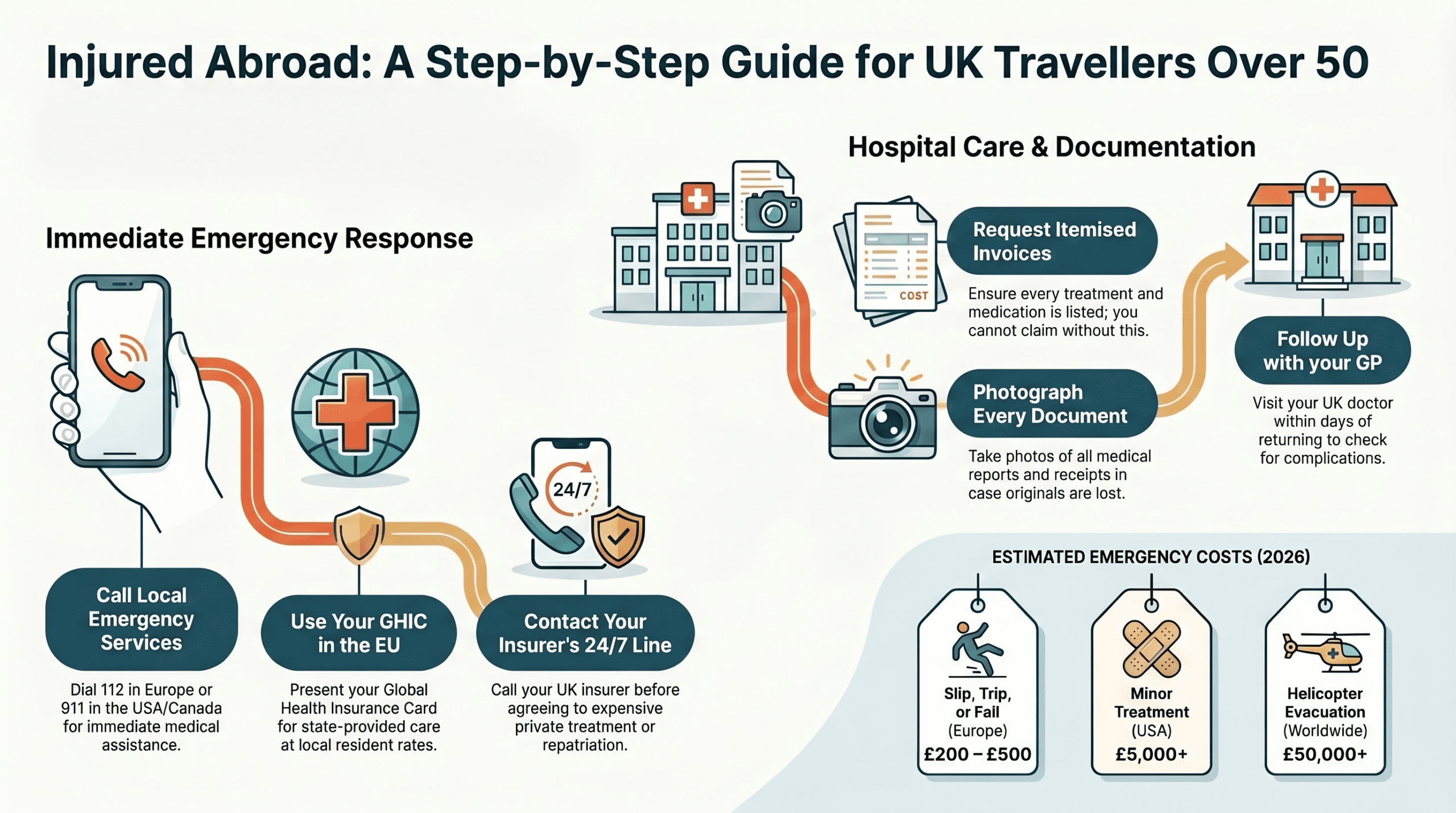

Immediate Steps After a Holiday Injury

If you have an accident whilst abroad, it’s vital to follow the correct procedures. For everything to organise before you fly, see our travel health checklist for over-50s. This ensures you heal as swiftly as possible and alerts relevant authorities if negligence caused your injury.

First priority: assess the severity. If the injury is obviously minor-a small cut or minor bruise-it may heal without professional help. However, if you’re in any doubt whatsoever, get it checked out immediately at a local clinic or hospital. Don’t wait or hope it improves on its own.

Seek medical attention. Find the nearest health facility-ask your hotel reception, call emergency services, or use Google Maps to locate a hospital or clinic. Medical staff abroad understand holiday injuries and can assess whether you need imaging, stitches, or specialist care.

Take detailed notes and photos. Once you’re treated, take photos of the injury itself and the location where it happened (if applicable). Document the date, time, and circumstances. This evidence is essential for insurance claims and compensation.

Report the incident to authorities. If negligence caused your injury-for example, a fall due to a poorly maintained hotel staircase or a traffic accident-report it to hotel management, the police, or the appropriate authority immediately. Get an incident report or reference number in writing.

Keep all medical records and receipts. Hold onto every receipt from doctors, hospitals, pharmacies, and diagnostic tests. Ask for copies of your medical notes, discharge summaries, and any prescriptions. These will be needed for your insurance claim or GP follow-up.

GHIC vs Travel Insurance: Which Covers What?

Many UK travellers believe the Global Health Insurance Card (GHIC) provides complete medical cover abroad. It doesn’t. Understanding what each covers-and their limits-could save you thousands of pounds.

What is a GHIC? Since Brexit, the European Health Insurance Card (EHIC) has been replaced with the Global Health Insurance Card (GHIC). It’s a free card issued by the NHS that entitles UK residents to state-funded healthcare in EU countries and several other destinations on the same basis as a local resident.

What the GHIC covers. The GHIC covers medically necessary treatment-any healthcare that cannot reasonably wait until you return to the UK. This includes emergency room visits, GP consultations, hospital admissions, treatment for long-term conditions, and routine maternity care. In most EU countries, this means free or reduced-cost treatment.

Critical gaps in GHIC cover. The GHIC does not cover medical repatriation (flying you back to the UK), private hospital stays, dentistry, routine optometry, or non-medical travel issues like cancelled flights or lost baggage. If you’re admitted to a private hospital in Europe, you pay the full cost-unless your travel insurance covers private treatment.

Travel insurance fills the gaps. Travel insurance protects you against costs the GHIC doesn’t cover: medical repatriation, private hospital fees, and emergency dental treatment. Most standard policies also cover trip cancellation, baggage loss, and legal liability.

Why travel insurance is essential for over-50s. As you age, the risk of needing emergency medical care increases. Falls, heart problems, and infections are common holiday hazards. A single episode of private hospital care in Spain can cost £1,100-£1,500 per night; in the USA, an intensive care unit stay might exceed £5,000 per night. Without travel insurance, you pay these costs yourself.

Travel Insurance for Over-50s with Pre-Existing Medical Conditions

If you have pre-existing conditions-such as diabetes, hypertension, arthritis, or heart disease-standard travel insurance may exclude you. Our complete UK guide to travel insurance with medical conditions compares specialist providers and explains the disclosure rules every traveller over 50 should know. Specialist over-50s policies exist, but they come at a premium.

Cost of specialist cover. In 2026, travel insurance for over-50s with pre-existing medical conditions costs approximately £40-£50 per day for a fortnight’s trip (around £280-£350 total). Some specialist providers offer annual policies for regular travellers, which may be more economical if you take multiple trips per year.

What you must disclose. When applying for travel insurance with pre-existing conditions, you must declare every relevant medical condition, medication, and any treatment you’ve had in the past 12 months. Failing to disclose means the insurer can refuse your claim. Be thorough in the medical history section.

Getting a quote. Use comparison websites, but also contact specialist insurers directly-they often offer better terms for people over 50 than mainstream providers. AllClear, InsureandGo, and Admiral all specialise in over-50s cover.

Check your policy before you travel. Before you book your holiday, confirm that your policy covers accidents and hospital care. Read the exclusions carefully. Some policies exclude high-risk countries or extreme activities-if you’re planning to hike or ski, check the activity list.

Medical Costs Abroad Without Insurance: A Comparison

If you travel without insurance and suffer a serious injury, the costs can be catastrophic. Here’s a realistic comparison of private hospital fees in popular holiday destinations.

| Treatment Type | Spain (Private) | Thailand (Private) | USA (Private) |

|---|---|---|---|

| ER consultation | £150-£300 | £55-£140 | £500-£2,000 |

| Hospital night (standard ward) | £1,100-£1,500 | £82-£547 | £5,000+ |

| Fracture treatment (X-ray, cast) | £800-£1,600 | £150-£1,000 | £2,000-£8,000 |

| Emergency surgery (appendix) | £3,000-£6,000 | £1,367-£5,468 | £15,000-£40,000 |

| Medical repatriation to UK | £5,000-£15,000 | £8,000-£25,000 | £10,000-£50,000 |

As you can see, costs vary dramatically by country. Thailand is significantly cheaper than Western Europe or the USA. However, even in Thailand, an emergency flight home can exceed £25,000. Private hospitals abroad require payment before discharge-your embassy will not pay your bill, and your family’s credit card won’t save you if funds run out.

Key takeaway: Travel insurance is not optional. A single night in a US hospital can exceed your annual travel insurance premium by 50-100 times.

Common Holiday Injuries for Over-50s: What to Watch For

Certain injuries are far more common in travellers over 50. Many minor injuries can be treated on the spot if you carry a properly stocked travel first aid kit. Knowing the signs of serious complications helps you decide when to seek urgent medical help.

Falls and fractures. Falls are the leading cause of injury-related death in people over 65. Even a minor fall can fracture a bone if you have osteoporosis. Seek medical attention if you cannot bear weight, have severe pain, obvious deformity, or numbness. In some countries, X-ray costs £100-£500; in the USA, £1,000-£2,000.

Food poisoning and gastroenteritis. Traveller’s diarrhoea is miserable but usually self-limiting. However, if you experience severe abdominal pain, blood in stool, signs of dehydration (dizziness, dark urine), or fever above 39C, seek medical help. Over-65s are at higher risk of serious complications.

Deep Vein Thrombosis (DVT). Long flights increase the risk of blood clots in your legs. DVT affects roughly 1 in 1,000 people annually in the UK, but risk rises with age. Warning signs include calf swelling, redness, warmth, or sharp pain in one leg. If untreated, a clot can travel to your lungs (pulmonary embolism), which is life-threatening. Wear compression stockings on long flights, move every 30 minutes, and stay hydrated.

Heat stroke and sun damage. Over-50s are more vulnerable to dehydration and heat-related illness. Symptoms include confusion, rapid pulse, high temperature, and lack of sweating. Seek urgent medical care if you suspect heat stroke. Sunburn may seem minor, but excessive UV exposure accelerates skin ageing and increases melanoma risk-use SPF 30+ and avoid midday sun.

Chest pain or shortness of breath. Never ignore chest pain, shortness of breath, or signs of a heart attack (pain in jaw, arm, or back; cold sweats). Call emergency services immediately-chest pain can develop rapidly after exertion, dehydration, or air travel.

When to Seek Urgent Medical Help Abroad

Some symptoms require immediate medical attention, regardless of whether you think the injury is serious. Tropical destinations also bring extra risk from insect bites and stings, where infections in older skin can spread quickly. Do not delay.

- Redness, swelling, or heat around a wound-signs of infection.

- High fever (over 38.5C) or fever lasting more than 48 hours.

- Loss of consciousness, fainting, or severe dizziness after a head injury.

- Bleeding that won’t stop after 15 minutes of direct pressure.

- Severe chest pain, shortness of breath, or signs of a stroke (facial drooping, arm weakness, speech difficulty).

- Severe allergic reaction (swelling of face, lips, or throat; difficulty breathing).

- Symptoms that worsen rapidly or significantly impact your ability to function.

Coordination with the NHS: What Happens When You Return

Once you’re fit to fly, the priority shifts to getting you home safely and ensuring continuity of care with the NHS.

Medical repatriation and fitness to fly. Before any repatriation flight, the treating hospital will assess whether you’re fit to fly. Severe fractures, recent surgery, respiratory problems, or heart conditions may mean you need medical escort or equipment during the flight. This increases the cost but ensures your safety.

NHS coordination. Healthcare providers abroad liaise with the NHS to ensure a hospital bed or suitable care is available when you land. If you’ve had major treatment abroad, your repatriating hospital sends detailed medical records to your local NHS trust.

Follow-up care with your GP. Within a few days of returning, contact your GP and provide copies of all medical records from abroad-discharge summaries, test results, medications prescribed, and any ongoing treatment recommendations. Your GP will review these and arrange any follow-up scans, medication adjustments, or specialist referrals needed.

Rehabilitation and ongoing support. The NHS offers rehabilitation, physiotherapy, and mental health support for people recovering from serious illness or injury abroad. If you suffered a fracture requiring months of recovery, your GP can refer you to physiotherapy. Ask about hospital discharge coordinators or community nurses if you need home support.

Making a Claim: Documentation and Next Steps

If you’ve paid for treatment abroad or incurred related costs, you may be able to claim from your travel insurance or pursue compensation for negligence.

Gather all documentation immediately. Before you leave the destination country, collect:

- Original receipts and invoices for all medical treatment, prescriptions, and hospital fees.

- Itemised invoices showing what was charged and why.

- Medical reports, discharge summaries, and copies of test results.

- Photographic evidence of the injury (early stages) and the location where it happened.

- Written incident report or police reference number if applicable.

- Witness contact details if others saw the accident.

Contact your insurer within days of returning. Do not delay. Most insurers require notification within 30 days of returning home or the incident occurring. Provide them with the incident date, description of what happened, and copies of all medical documentation. Ask them to confirm cover before you submit a claim.

Submit your claim with complete evidence. Insurance claims are denied most often because of missing documentation, not because the incident isn’t covered. Submit:

- A written statement describing the incident and your injury.

- All receipts and invoices (originals if possible).

- Medical reports and records.

- Photos and witness statements.

- Proof of payment (credit card or bank statements).

Claiming compensation for negligence. If your injury was caused by someone else’s negligence-a dangerous hotel staircase, poor medical care, or a traffic accident caused by another driver-you may be entitled to compensation beyond your insurance claim. Consult a solicitor specialising in holiday accident claims; many offer free initial consultations. Keep all evidence and correspondence with the responsible party.

Frequently Asked Questions

Can I claim on the NHS for treatment I received abroad?

No. The NHS does not reimburse treatment you paid for abroad. Travel insurance is your only recourse – or compensation from the responsible party if negligence caused your injury.

Will my GHIC cover me if I travel outside the EU?

The GHIC covers EU countries and a small number of other nations (Iceland, Norway, Liechtenstein, and Switzerland). If you travel to the USA, Thailand, Egypt, or other non-covered destinations, you must have travel insurance. The GHIC is useless outside its designated countries.

What if I am refused treatment abroad because I cannot pay upfront?

Emergency care cannot legally be refused in most countries, even if you cannot pay immediately. However, private hospitals will demand payment before discharge. Contact your insurer’s emergency line – they may be able to guarantee payment directly to the hospital, avoiding a large upfront cost.

What happens if my injury gets worse after I return home?

Inform your GP immediately. Complications from untreated infections, blood clots, or fractures can develop weeks after an injury. Your NHS care is free, and your doctor can arrange imaging, antibiotic treatment, or surgery as needed. Send your GP copies of the medical records from abroad so your UK doctor understands your full medical history.

Key Takeaways

- If you’re injured on holiday, seek immediate medical attention. Do not delay or hope it improves.

- The GHIC covers state-funded healthcare but not medical repatriation or private hospital stays. Travel insurance fills this critical gap.

- For over-50s with pre-existing conditions, specialist travel insurance costs £280-£350 for a fortnight but can save you tens of thousands of pounds.

- Medical costs vary drastically: a hospital night costs £1,100-£1,500 in Spain, £82-£547 in Thailand, and £5,000+ in the USA without insurance.

- Collect all medical records, receipts, photos, and incident reports before you leave the destination country-you cannot obtain them remotely later.

- Contact your travel insurer within days of returning home, not weeks. Most claims are denied due to missing documentation, not lack of cover.

- Complications from holiday injuries can develop weeks later. Inform your GP of any treatment you received abroad so they can monitor your recovery.

What to Do Next

Before your next holiday, review UK government guidance on travel insurance and get a travel insurance quote from a specialist over-50s provider. If you’re travelling within the EU, apply for a free GHIC at least two weeks before you travel. And if you’ve been injured on a previous holiday, use the lessons you’ve learned-being injured abroad is frightening, but with the right insurance and knowledge, you can manage it and recover well.

Useful Resources and Sources

- UK Global Health Insurance Card (GHIC) – GOV.UK – Apply for your free GHIC and check which countries are covered.

- Foreign Travel Insurance – GOV.UK – Official guidance on travel insurance requirements and what to look for in a policy.

- Healthcare Abroad – NHS.uk – Comprehensive information about accessing healthcare overseas and returning to the UK.

- Association of British Insurers (ABI) – Expert advice on choosing travel insurance and understanding coverage.

- Emergency Help for British Nationals – FCDO – Contact information and guidance if you need consular assistance abroad.

Disclaimer: This article is for information only. Always consult your GP or a qualified healthcare professional before making health decisions. If you are injured on holiday, seek immediate medical attention from a local healthcare provider. This guide is not a substitute for professional medical or legal advice. For specific questions about your travel insurance cover or medical condition, contact your insurer or GP directly.

Join the community

For more practical travel health advice for over-50s, join our Facebook community where we share weekly tips, NHS updates, and reader stories.