Travel Insurance with Medical Conditions: Complete UK Guide for Over-50s

If you’re over 50 with a pre-existing health condition, securing travel insurance shouldn’t feel impossible. The truth is, specialist providers in the UK now offer comprehensive cover for everything from diabetes and heart disease to arthritis and COPD. But not all policies are created equal, and premiums can vary dramatically depending on your condition, age, and destination. This guide reveals exactly what you’ll pay, which providers offer the best value, and how to find cover that genuinely protects you abroad.

We’ll compare costs from leading UK insurers, explain what coverage you actually need, and walk you through the medical screening process so there are no surprises when you claim. Whether you’re planning a week in the Mediterranean or a long-haul adventure, you’ll find practical, evidence-based advice to travel with confidence.

Travel Insurance Costs: What You’ll Actually Pay in 2026

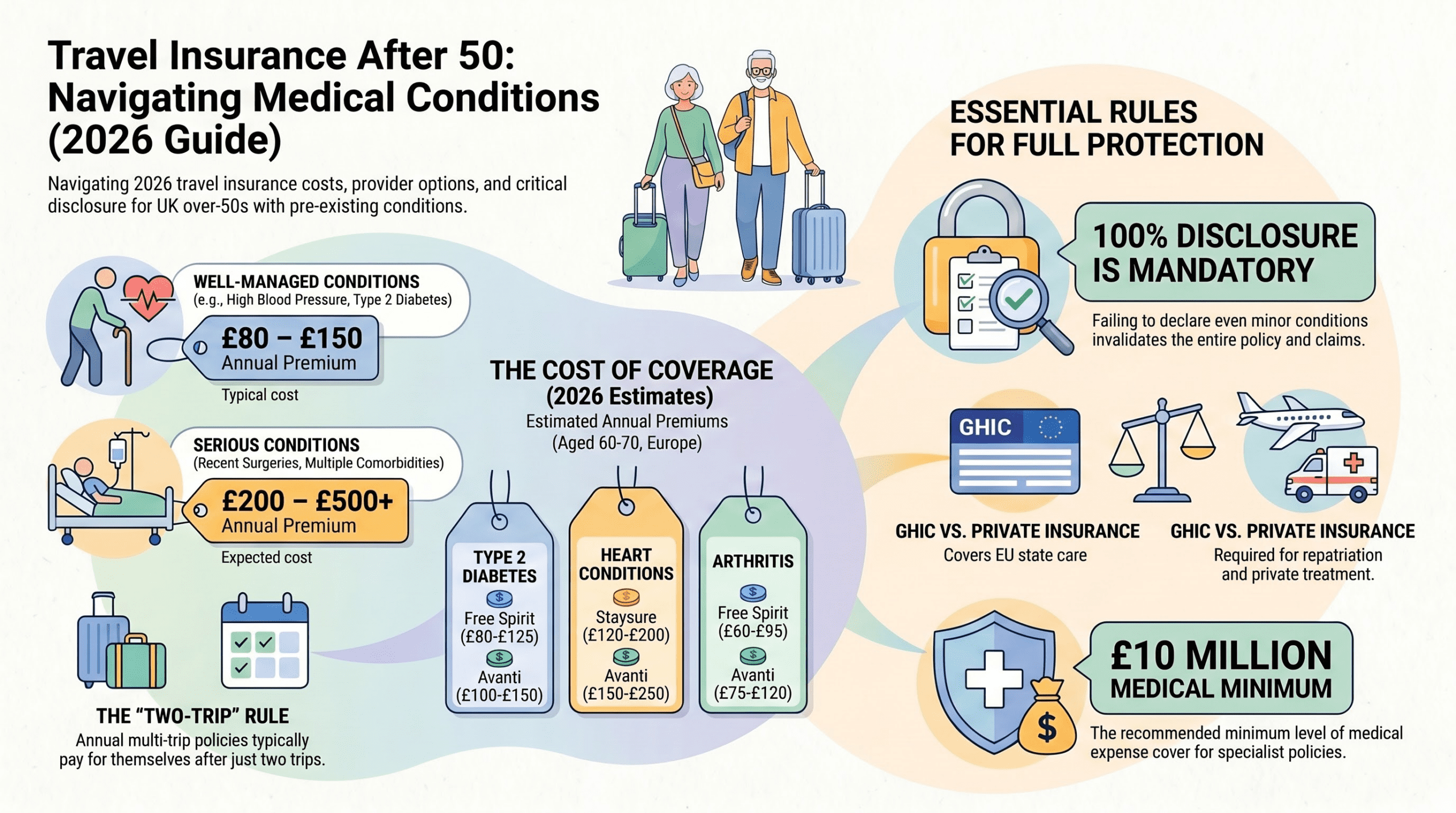

Medical conditions push up premiums – but by how much depends on your age, condition severity, and trip length. For a healthy 50-year-old, standard annual multi-trip cover costs 40-80. Add a well-managed condition like type 2 diabetes or high blood pressure, and you’re looking at 80-150. Serious conditions such as recent cancer treatment, heart surgery, or multiple comorbidities can reach 200-500+ per year, depending on the provider.

Single-trip policies are always cheaper than annual cover but don’t suit frequent travellers. A one-week trip for a 60-year-old with diabetes might cost 35-60, while the same person paying for annual cover would spend 100-180 and make the investment back after just two trips.

Specialist Provider Comparison Table: Annual Multi-Trip Premiums (2026)

The table below shows typical annual multi-trip premium ranges for four common conditions across five leading UK specialists. Exact prices depend on your age, destination, and medical details – always request a quote.

| Provider | Type 2 Diabetes | Heart Condition | Arthritis | COPD |

|---|---|---|---|---|

| AllClear | 95-140 | 140-220 | 70-110 | 130-180 |

| Staysure | 85-130 | 120-200 | 65-100 | 125-170 |

| Avanti | 100-150 | 150-250 | 75-120 | 140-190 |

| InsureandGo | 90-135 | 135-210 | 70-105 | 128-175 |

| Free Spirit | 80-125 | 130-190 | 60-95 | 120-165 |

Figures based on 2026 quotes for ages 60-70, travelling within Europe. Prices vary by medical history, additional conditions, and destination risk. Always obtain a personal quote.

Why Costs Vary: The Hidden Factors

Insurers don’t just look at your condition – they assess severity, how long you’ve had it, and whether it’s stable. Type 2 diabetes controlled with diet costs far less than insulin-dependent diabetes with complications. A heart condition 10 years post-event is lower risk than one diagnosed last year. High-altitude destinations, countries with expensive healthcare, and long-haul trips all push premiums higher.

Watch: The 2026 Travel Insurance Guide for Over-50s With Medical Conditions

In this short cinematic guide, you’ll see what travel insurance with medical conditions actually costs in 2026, why declaring every condition matters, how the medical screening process works, and how to compare specialist UK providers like AllClear, Staysure, Avanti, Free Spirit and Saga.

What Travel Insurance Actually Covers (And What It Doesn’t)

Travel insurance with medical conditions protects you against emergency medical costs abroad. This includes hospital treatment, emergency surgery, medication, and repatriation back to the UK if needed. A typical policy covers 1-5 million in medical expenses, though costs vary by provider and condition.

Critical distinction: insurance covers emergency medical treatment for existing conditions, not routine care or treatment you could have delayed until home. If your condition flares unexpectedly while abroad, you’re covered. If you travel to seek specialist treatment, you’re not.

What Standard Policies Always Cover

- Emergency hospital admission and treatment

- Emergency surgery and anaesthesia

- Emergency ambulance and air ambulance to hospital

- Emergency dental treatment (up to limit)

- Medical repatriation to the UK

- Prescribed medications needed during your trip

- 24/7 emergency helpline staffed by medical professionals

What Medical Policies Often Exclude

- Routine check-ups or preventive care

- Travel to countries with health alerts (unless specifically added)

- Conditions you didn’t declare (non-disclosure voids your policy)

- Travel against your doctor’s advice

- Claims arising from not taking prescribed medication

- Treatment for conditions not declared in your medical screening

Key Takeaways

- Annual multi-trip cover with medical conditions costs 80-150 for well-managed conditions, rising to 200-500+ for serious or recent diagnoses.

- Always declare every pre-existing condition – omitting information voids your entire policy and leaves you uninsured abroad.

- Specialist providers like AllClear, Staysure, and Free Spirit cover over 1,000 conditions. Mainstream insurers typically won’t.

- Single-trip policies suit one-off holidays; annual cover is better value if you travel more than twice yearly.

- Emergency cover is essential – medical evacuation from abroad can cost 10,000-100,000+ without insurance.

Understanding the Medical Screening Process

Before cover begins, insurers ask detailed questions about your health. This isn’t to refuse you – it’s to price your risk accurately and ensure you’re truly covered.

You’ll be asked about previous hospital admissions, current medications, whether you’ve had investigations or specialist referrals, and whether your condition is stable. Some insurers request a GP’s medical report for serious conditions. This takes 1-2 weeks but is worth the wait to guarantee you’re not voiding your policy through incomplete disclosure.

Medical Screening Questions You’ll Face

- Have you had any inpatient or outpatient treatment in the last 2-5 years?

- Have you had any surgery, investigations, or specialist referrals?

- What medications do you take, and what conditions are they for?

- Are you currently under investigation for any new symptoms?

- Have you had any unplanned hospital admissions?

- Are you a current or former smoker?

- Do you have any mental health conditions?

Answer everything honestly. Many people think mild, well-managed conditions “don’t count” – they absolutely do. If you’ve ever taken medication for it, had a test, or been referred to a specialist, you must declare it. Insurers have access to your GP records, and if they discover non-disclosure later, they’ll reject claims and potentially blacklist you for future cover.

Travel Insurance for Specific Medical Conditions

Type 1 and Type 2 Diabetes

Diabetes ranks among the easiest pre-existing conditions to insure. Most specialists cover both type 1 and type 2, whether controlled by diet, tablets, or insulin. Premiums range 80-140 annually for well-controlled diabetes, rising to 150-200 if you’ve had recent complications like neuropathy or kidney issues.

Travelling with diabetes means managing different meal times, time zones, and activity levels. Ensure your travel insurance covers emergency treatment for severe hypo- or hyperglycaemia, and carry at least double your usual medication supply. Store insulin in a cool bag; heat degrades it rapidly. Request written confirmation from your insurer that insulin and glucose monitors are covered before you travel. For related reading on metabolic risk factors, see our guide to lowering blood pressure naturally.

Heart Disease and Cardiovascular Conditions

Premiums for heart conditions are higher – typically 130-220 annually – because medical emergencies can develop suddenly and require expensive emergency care. Conditions covered include coronary artery disease, atrial fibrillation, heart failure, and previous heart attacks or stents.

Your insurer will ask when your event occurred, what treatment you’ve had (bypass, angioplasty, medications), and whether your condition is stable. Travel within 2-3 months of a heart event is risky and often excludes you from cover. Wait at least 3-6 months, get your cardiologist’s clearance, and carry a copy of your latest ECG and medical report.

Long flights increase risk of blood clots; wear compression socks, move regularly, and stay hydrated. Inform your insurer of the flight duration so they can assess whether evacuation cover is needed. Our overview of reducing the risks of hypertension explains why managing blood pressure matters particularly before long-distance travel.

Arthritis and Joint Conditions

Arthritis is one of the cheapest conditions to insure, with premiums from 60-120 annually. Osteoarthritis, rheumatoid arthritis, and post-surgical joint problems are all routinely covered by specialists.

Travel comfort matters more than cover for arthritis. Request airport assistance, aisle seats for long flights, and accommodation near sites you wish to visit. Insurance covers flare-ups requiring emergency treatment, but most arthritis claims are for cancelled trips due to acute pain – ensure your policy includes trip cancellation cover for medical reasons.

COPD and Respiratory Conditions

Chronic obstructive pulmonary disease (COPD), asthma, and other respiratory conditions are well covered, with premiums from 120-190 annually. Insurers need to know your lung function (FEV1 percentage), how often you need hospital admissions, and whether you use home oxygen.

Destination matters hugely. High-altitude travel risks acute exacerbation if you have COPD. Heat, humidity, and poor air quality can trigger asthma. Discuss your destination with your respiratory consultant before booking. Arrange any oxygen or nebuliser equipment through your insurer in advance; many policies include this, but you must notify them first.

Cancer: During and After Treatment

Travel insurance for cancer is expensive – 250-500+ annually during active treatment – because the risk of medical emergencies is high. Cancer Research UK advises most patients to avoid travel during chemotherapy or radiotherapy due to infection risk and unpredictable side effects.

Post-treatment, premiums drop significantly once you’ve been cancer-free for 1-2 years. Declare the cancer type, date of diagnosis, treatments completed, and any ongoing monitoring. Many insurers exclude travel to countries with inadequate oncology services or high infection risks. Check this before booking.

Mental Health Conditions

Depression and anxiety are increasingly covered by specialists. Premiums are usually 80-150 annually if the condition is stable and treated. You’ll be asked about current medication, any hospital admissions, and whether you’ve had time off work recently.

A key benefit for mental health is trip cancellation cover – if your condition deteriorates and your doctor advises against travel, you can cancel without losing money. Ensure your policy covers this. Some insurers exclude mental health cover if you haven’t been stable for at least 3-6 months, so disclose honestly about your recent history.

GHIC and EHIC: What They Do and Don’t Cover

The Global Health Insurance Card (GHIC) replaced the EHIC for UK citizens after Brexit. Both provide limited emergency cover in EU and EEA countries, but they are not travel insurance and should never replace it.

What GHIC/EHIC Covers

- Emergency hospital admission and treatment in EU and EEA countries

- Some prescription medications required during your stay

- No cost for services (care is free at point of use in most EU countries)

Critical Gaps GHIC Doesn’t Cover

- Private medical treatment or private hospitals

- Repatriation to the UK (even emergency flights home)

- Medical evacuation or air ambulance

- Travel outside the EU/EEA

- Claims because your condition wasn’t declared to travel insurance

- Cancellation, lost baggage, or trip interruption

A medical evacuation flight from Mediterranean coast to UK costs 8,000-30,000. GHIC covers nothing. Travel insurance covers everything. This is why the Association of British Insurers (ABI) urges every traveller – especially those with medical conditions – to buy comprehensive insurance regardless of GHIC status.

Choosing the Best Travel Insurance Provider for Your Condition

Not all specialists are created equal. Before committing to a policy, compare these six factors directly.

1. Medical Conditions Covered

AllClear and Free Spirit cover over 1,300 pre-existing conditions each. Staysure and Avanti have more selective lists but are often cheaper for common conditions. Use their online medical checker – if your condition doesn’t appear, you might be declined or heavily loaded. Get a quote before assuming you’re uninsurable; many insurers offer cover not visible on their website.

2. Medical Expense Limit

Standard limits are 1-2 million for European travel. USA and Asia require higher limits; check whether a 5 million option is available without extra cost. Once you know your likely destination, confirm the limit covers likely scenarios – particularly if you might need air ambulance evacuation (typically 10,000-100,000).

3. Exclusions and Conditions

Read the policy exclusions table carefully. Some insurers exclude certain destination countries, high-altitude travel, or claims arising from not taking prescribed medication. Others exclude travel against medical advice. Check whether trip cancellation due to your medical condition is covered – this is valuable if your condition deteriorates before departure.

4. Emergency Assistance Quality

All specialists offer 24/7 helplines, but some are UK-based medical professionals; others outsource to call centres. Staysure, AllClear, and Free Spirit have positive reviews for medical helpline quality. Read recent customer reviews specifically mentioning emergency use – this matters far more than features you may never need.

5. Repatriation and Evacuation

Ensure your policy covers emergency repatriation (flying you home in a commercial plane) and emergency evacuation (air ambulance to nearest adequate hospital). The difference is critical. Repatriation typically costs insurers 2,000-5,000; evacuation can exceed 100,000. Some policies limit evacuation to life-threatening situations only. Clarify exactly what’s covered before a claim arises.

6. Premium vs. Deductibles

A cheap premium often means a high deductible (excess). You might pay 90 annually but face a 250 claim excess, meaning you pay the first 250 of any claim yourself. Compare the true cost: annual premium + likely deductible. A 120 annual policy with no excess is better value than 85 with a 200 excess if you claim.

What to Check Before You Buy: Essential Questions

Use this checklist before purchasing any policy.

Condition and Coverage

- Is my specific condition (or all my conditions) covered? Get written confirmation.

- Are any related complications excluded? (e.g., diabetes and kidney disease)

- What’s the maximum time since my condition started that I can claim? (Some insurers exclude claims within 12 months of diagnosis.)

- Is travel within 2-3 months of a serious event (surgery, heart attack, cancer diagnosis) permitted?

Coverage Limits and Costs

- What is the maximum medical expense limit for my destination?

- Is repatriation covered? Is evacuation covered?

- What’s the deductible (excess) per claim, and is it waived for emergency treatment?

- Are prescription medications covered? Up to what limit?

- If my destination is high-altitude or high-risk, is cover still provided?

Exclusions and Restrictions

- Are there any excluded countries or regions?

- Is trip cancellation covered if my condition worsens before departure?

- Am I covered if I travel against medical advice?

- What happens if my condition changes between buying the policy and travelling?

- Can I extend the policy while abroad if my trip runs longer?

Medical Screening and Underwriting

- What medical information do you need from me? A GP report, or just a questionnaire?

- How long does underwriting take? (Typically 5-10 working days.)

- If my GP report takes longer to obtain, will you hold my quote?

- If I’m declined or heavily loaded, what’s your appeals process?

Claims and Support

- Is the emergency helpline UK-based and staffed by medical professionals?

- Can I claim through the insurer directly, or must I pay upfront and claim later?

- What documents do you need for a claim? (Request a claims checklist in advance.)

- What’s your average claims payment time?

Practical Tips for Travelling Safely with Medical Conditions

Before You Leave

- Speak to your GP at least 8 weeks before travel. Our healthy living guide for longer lives has more on preparing for travel, activity, and everyday health after 50. Ask whether your destination is safe for your condition, whether your current medication is appropriate, and whether you need any preventive measures (e.g., DVT prophylaxis for long flights post-surgery).

- Carry a medical summary letter from your GP. This includes your diagnoses, medications (with doses), any recent investigations, and emergency contact details. It’s invaluable abroad and helps local doctors understand your history quickly.

- Take double your usual medication supply. Checked luggage should contain a copy of prescriptions or a letter from your pharmacy proving the medication is prescribed to you – some countries restrict certain drugs, and this proof helps customs.

- Ensure your travel insurance is active before departure. Cover only starts once your quote is accepted and payment clears, typically within 24 hours. Don’t assume cover is live just because you’ve completed the online form.

- Notify your insurer of any new symptoms or diagnosis before travelling. If your condition changes after you’ve applied but before you depart, tell your insurer immediately. Travel against undisclosed medical changes might void your policy.

During Travel

- Carry your insurance policy documents and emergency helpline number. Save the number in your phone, write it in your travel documents, and give it to a family member at home. Many people have travel insurance but can’t find the helpline number when they need it.

- Store medications appropriately. Insulin requires cool storage (2-8C). Carried on flights, you can transport it in a cool bag or request a refrigerator at your accommodation. Some conditions require specific storage temperatures; ask your pharmacy before departure.

- Stay familiar with your destination’s healthcare system. Research the nearest hospital to your accommodation. In Europe, 112 is the emergency number; other countries differ. Know which hospitals your travel insurance recognises (your insurer’s helpline can confirm this).

- Maintain your medical routine. Travellers often skip medication or alter timing due to time zones and unfamiliar routines. Set phone reminders. Take medication at your home time for the first few days, then gradually shift to local time. Never suddenly stop or skip doses.

- Consider wearing a medical alert bracelet or card. If you collapse or become unconscious, emergency responders will know about your conditions and medications immediately. Carry a card in the local language if possible.

In a Medical Emergency Abroad

- Call emergency services immediately if life-threatening. In most of Europe, it’s 112. Don’t worry about the cost – insurance covers it. Get medical help first, worry about paperwork later.

- Contact your travel insurance helpline as soon as it’s safe to do so. They’ll confirm cover, advise on next steps, and often arrange direct payment to hospitals (saving you upfront costs). Tell them everything: your condition, what happened, and what treatment you’re receiving.

- Inform medical staff of your conditions and medications immediately. Don’t assume they know about your NHS records or previous treatment. Give them your GP letter (mentioned earlier), medication list, and allergies. Language barriers? Use a translation app or ask your insurer’s helpline to translate key information.

- Keep all documents: receipts, medical reports, prescriptions, and correspondence. You’ll need these to claim. Ask the hospital for an itemised invoice showing treatment, costs, and dates.

- Follow medical advice completely. If a doctor advises hospitalisation, admit yourself. If they recommend follow-up care after discharge, attend it. Insurance policies can deny claims if you ignore medical advice.

Frequently Asked Questions

Do I have to declare every pre-existing condition?

Yes, absolutely. Insurers have access to your GP records and can refuse claims if you’ve omitted information. If you’ve ever taken medication for a condition, been referred to a specialist, or had tests related to it, declare it. When in doubt, ask your insurer before applying.

How much more does travel insurance cost with a medical condition?

Premiums vary widely depending on the condition, your age, and the destination. For well-controlled conditions like high blood pressure or high cholesterol, premiums may increase by 20 to 50 per cent. For more complex conditions such as cancer (in remission), heart disease, or diabetes, premiums can double or triple. Specialist insurers often offer better rates than general providers for people with medical conditions.

Which travel insurance companies are best for pre-existing conditions?

Specialist providers such as AllClear, Staysure, InsureandGo, and Free Spirit tend to offer more competitive premiums and better coverage for pre-existing conditions than mainstream insurers. Comparison websites like MoneySupermarket and ComparetheMarket allow you to filter by medical conditions. Always check the policy wording carefully – the cheapest quote may have exclusions that leave you underinsured.

Will travel insurance refuse me because of my condition?

Unlikely, if you have a condition that specialists insure. Conditions like diabetes, heart disease, arthritis, COPD, and mental health issues are routinely covered. Very rare conditions, terminal cancer, or very recent serious diagnoses might be declined by some insurers, but others often will cover them (usually at a higher premium). You might be “loaded” (a surcharge applied), but outright refusal is unusual. Always ask – don’t assume.

What’s the difference between travel insurance and GHIC?

GHIC provides limited emergency cover in EU/EEA countries but doesn’t cover repatriation, evacuation, trip cancellation, or travel outside Europe. Travel insurance covers all of this, plus emergency medical costs worldwide, and works alongside GHIC (both together give maximum protection). Never rely on GHIC alone if you have a medical condition.

Can I get travel insurance after a cancer diagnosis?

Yes, though premiums will be higher and coverage may have some exclusions. Several specialist insurers cover cancer patients and cancer survivors. Premiums depend on the type of cancer, how recently you were diagnosed or treated, and whether you are in remission. Some policies exclude claims related to the cancer but cover everything else. Always disclose your full diagnosis and treatment history to avoid policy invalidation.

Can my insurance cover me if my condition worsens during the trip?

Yes, as long as the worsening is unexpected and you’ve declared the original condition. If you had a known heart condition and suffered a heart attack abroad, that’s covered. If your arthritis flared painfully, requiring emergency treatment, that’s covered. But if your condition is already known to be deteriorating and you travel despite medical advice against it, claims might be denied.

How long does medical underwriting take?

Online quotes for common conditions (if no GP report is needed) can confirm cover within minutes. If a GP report is required, allow 5-10 working days for your doctor’s surgery to write it, then another 1-2 days for the insurer to assess it. Plan ahead – don’t apply for insurance a week before your trip if you need a medical report.

Am I covered if I travel against my doctor’s advice?

Most insurers exclude claims arising from travel against medical advice. If your GP specifically advises against travel and you go anyway, and your condition deteriorates, the claim might be refused. Always discuss your destination and trip plans with your GP. If they clear you, get this in writing – it’s useful if a claim dispute arises later.

What if my medical condition changes after I’ve bought my policy?

Tell your insurer immediately. Depending on the change, they might adjust your cover at no extra cost, ask for an updated GP report, or in rare cases, reconsider cover. New diagnoses must be declared before you travel – travelling with an undisclosed new condition risks voiding your entire policy.

Will I be able to claim for prescription medication abroad?

Most policies cover emergency prescription medications needed during your trip, up to a limit (often 200-500). Routine medications you take at home are usually covered if prescribed before travel and needed to manage your pre-existing condition. Check your policy document under “Medication Cover” – it’s often missed but valuable.

What happens if I need emergency treatment in a private hospital abroad?

Travel insurance covers emergency treatment in private hospitals if the private facility is the nearest adequate hospital available. If a public hospital is available and closer, insurers might expect you to use that instead. Discuss with your insurer’s emergency helpline immediately if you’re admitted to private care – they’ll confirm cover and arrange payment.

Useful Resources and Sources

The following organisations provide trusted information on travel insurance, healthcare abroad, and medical conditions.

- NHS.uk – UK health information and GP finder for pre-travel advice.

- Association of British Insurers (ABI) – Trade body for UK insurance; provides consumer guidance on travel insurance standards and complaints.

- Financial Conduct Authority (FCA) – UK financial regulator. Check if your insurance provider is FCA-regulated.

- GOV.UK Travel Advice – Government information on GHIC, travel to EU countries, and healthcare abroad.

- Age UK – Charity providing support and advice specifically for people over 50, including travel safety.

- Which? – Independent consumer testing organisation; regularly publishes travel insurance reviews and comparative data.

- MoneyHelper – Government-backed money guidance including travel insurance information.

Summary: Your Travel Insurance Action Plan

Travelling abroad with a pre-existing medical condition is safe and achievable with the right insurance and preparation.

Your Next Steps

- Identify your conditions: Compile a list of every diagnosis, medication, and investigation you’ve had. Include dates if you have them.

- Consult your GP: Confirm that your destination is safe and discuss any preventive measures (DVT prophylaxis, vaccinations, altitude concerns).

- Get quotes from specialists: Use online comparison tools or contact AllClear, Staysure, Free Spirit, Avanti, and InsureandGo directly. Be honest in medical screening – answers determine cover.

- Check the small print: Use the checklist above to review exclusions, limits, deductibles, and emergency helpline quality.

- Request a GP medical report if needed: If underwriting requires one, ask your surgery to send it directly to the insurer (this speeds things up).

- Buy cover at least 2 weeks before departure. This gives time for underwriting and problem-solving if anything is queried.

- Save your insurer’s emergency helpline number in your phone and give it to a family member. Carry a printed copy in your wallet.

- Travel with confidence. You’re covered, prepared, and ready to enjoy your adventure.

Important Disclaimer:

This article is for information only and does not constitute medical, financial, or legal advice. Always consult your GP or a qualified healthcare professional before travelling with a medical condition, and carefully read your insurance policy documents before purchase. Information about premiums, conditions covered, and provider features was accurate as of March 2026 but may change. Always contact your chosen insurer directly for current quotes, eligibility, and terms. The Best of Health accepts no liability for claims denied due to incomplete disclosure or policy misunderstanding. Travel safely.